After stabilizing through much of 2024 following a period of shocks, the global economic landscape has been altered by new trade policy measures and countermeasures. For Slovakia, uncertainty has fundamentally returned due to geopolitical tensions, and domestic fiscal consolidation. These include both implemented and planned measures totaling approximately €5 billion over the next two years. The fiscal measures drew heightened attention from the public, especially lower-income households, and from businesses in the trade and services sectors. This renewed unpredictability is a significant factor hindering economic recovery and affecting decisions by households and firms regarding consumption, investment, and employment.

Economic growth

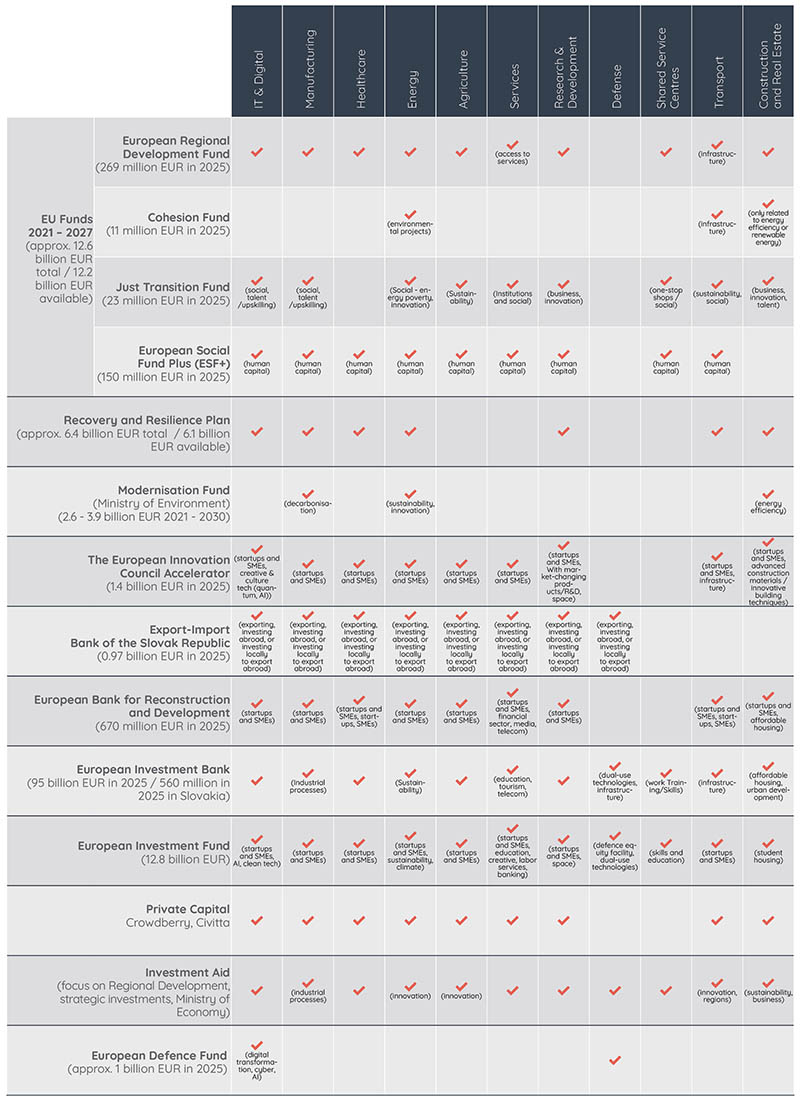

According to the National Bank of Slovakia’s Spring 2025 forecast, economic growth in Slovakia is expected to slow to 1.9% in 2025 and stay at 1.9% in 2026, a downward revision from winter 2024. Growth will be supported by increased EU funds absorption, recovering foreign demand, and expanding automotive production. Consumer demand should also strengthen as income growth outpaces inflation. While the end of Recovery and Resilience Facility (RRF) funding will reduce EU fund absorption, this will be mitigated by faster absorption of regional development funds from the 2021–2027 budget.

The IMF’s reference forecast projects Euro Area growth at 0.8% in 2025 and 1.2% in 2026. Heightened uncertainty is expected to keep growth subdued in the Euro area. The OECD notes that global growth is projected to weaken, although it remained resilient in 2024, supported by strong expansion in the United States and several large emerging-market economies, including China.

Inflation

Slovakia’s annual HICP inflation rate is expected to accelerate temporarily to 4.3% in 2025. It is then projected to fall to 2.9% in 2026. This projection assumes that household energy prices remain frozen. The temporary acceleration in 2025 is largely due to uncertainty and tax changes, with their impact most evident in services and administered prices.

Globally, headline inflation is projected to decline to 4.3% in 2025 and 3.6% in 2026, slightly slower than previously forecast. In the Euro area, inflation is gradually easing toward the ECB’s 2% target, with headline inflation at 2.5% in early 2025. However, core inflation remains above target in several economies.

Labor Market Conditions

Employment in Slovakia is estimated to stay at current levels, supported by inflows of foreign workers. Aging demographics will pressure wages, with average nominal wage growth projected at nearly 5% annually from 2025-2027. Unemployment is projected at 5.2% in 2025 and 5.5% in 2026.

Banking

2024 stress tests (based on end-2023 data) showed the banking sector remains resilient, with a moderate 160 basis point decrease projected through 2026. Based on the synthesis of 25 sustainable banking supply and demand side indicators, Slovakia has the lowest total score (87 out of a possible 200) among the eight CEE countries included in the ranking, suggesting a less favorable environment for sustainable banking growth compared to its regional peers.

Export

Export

The outlook for foreign demand for Slovak products continues to deteriorate, especially in 2026, partly driven by the ongoing slowdown in Germany’s industrial output. However, exports are projected to recover this year, primarily supported by a strengthening automotive sector and a resurgence in consumer spending across the EU. Foreign demand for Slovakia is projected to grow by 2.4% in 2025 and 2.9% in 2026, although this is a downward revision from the winter 2024 forecast.

The Impact of US Tariffs on the Slovak Economy

The National Bank of Slovakia’s Spring 2025 forecast estimates the imposition of US tariffs to have significant negative impacts on Slovakia. Small, highly open, and export-driven economies like Slovakia are particularly vulnerable to external shocks like trade wars. Despite limited direct US trade links (4.2% of exports), Slovakia’s vulnerability stems from its integration into European, particularly German, value chains.

Cumulative GDP growth is estimated to fall by almost 3% by the end of 2027, representing a loss of more than €3 billion. Slovak exports are projected to experience a €5 billion drop by 2027 compared with a scenario without tariff increases. The Slovak economy is estimated to lose around 20,000 jobs over the next three years. The sector most affected by the slowdown is the manufacturing industry, especially the machinery and automotive industries, due to their export orientation and dependence on global demand.

The Policy Outlook and Recommendations by IMF

- Trade Policy: Urgent international cooperation is needed to avoid further retaliatory barriers, promote transparent policies, and potentially pursue agreements that reduce tariffs.

- Monetary Policy: Central banks should remain vigilant. Gradual policy rate reductions could continue if underlying inflation and expectations remain subdued.

- Fiscal Policy: Credible fiscal adjustment plans are necessary to ensure debt sustainability and preserve room for future shocks. This involves containing spending and enhancing revenues. For Slovakia, this involves addressing the impacts of recent consolidation and ensuring additional efforts are made, while maintaining fiscal transparency to support credibility.

- Structural Reforms: Ambitious reforms are needed to strengthen growth, especially amid trade pressures. This includes regulatory reforms to boost competitiveness and productivity, improving capital/labor markets, and supporting digital infrastructure and skills. Rising protectionism reinforces the need for such reforms.

- Financial Stability: Robust prudential policies and vigilance are crucial given uncertainty and volatility. Measures like releasing countercyclical buffers, targeted liquidity support, and managing exchange rate volatility may be appropriate depending on conditions. High debt levels and substantial refinancing needs pose risks.

Marcela Gocmanová, Consultant, PA Matters s.r.o.

Follow us